Lihat juga

31.03.2026 12:54 AM

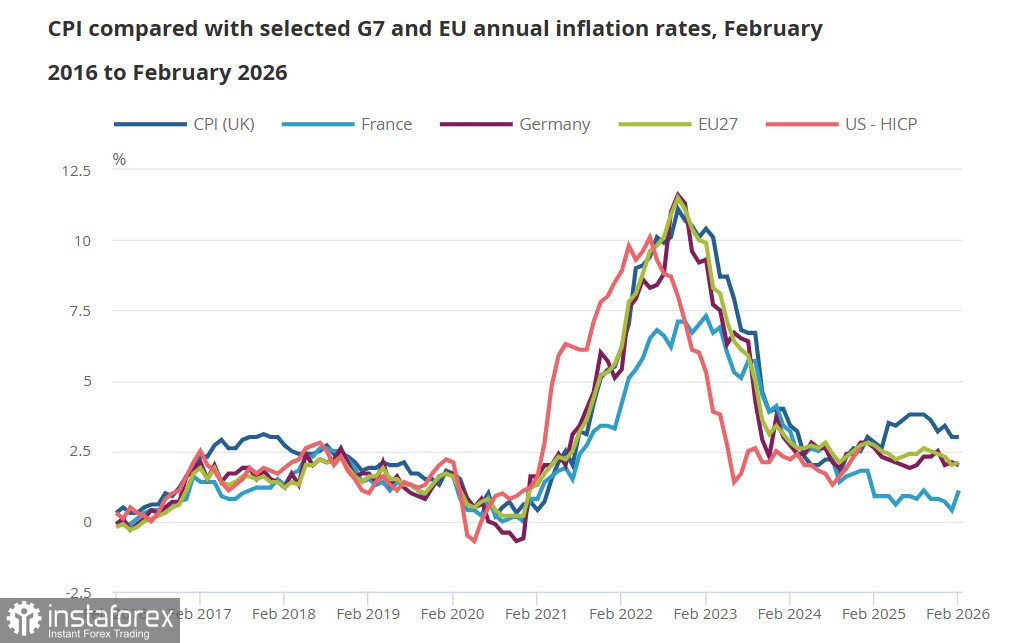

31.03.2026 12:54 AMInflation in the UK remained at 3% in February, which is now completely outdated, as it does not account for the price surge in March due to the energy market crisis. At the same time, even under these stable conditions, core inflation rose from 3.1% to 3.2%, which almost certainly indicates that all price components will grow in March.

Comparing price dynamics between the UK and EU countries, the overall price level at the beginning of March remained significantly higher in the UK. While ECB forecasts suggest a rate hike as early as April, the latest market expectations for the Bank of England imply three rate increases this year.

What does the war in the Middle East mean for the UK economy? It is clear that economic growth will slow down, which, in turn, will lead to a decrease in tax revenues – falling consumer spending reduces VAT income, struggling businesses lead to lower corporate tax revenues, and slowing wage growth suppresses future income from income tax. In the worst-case scenario, all of this will be compounded by rising unemployment, business closures, and increasing social welfare costs.

With GDP growth slowing, actions to ease financial conditions are in demand. But not in this case, as the rising inflation, which is inevitable, will lead to increasing interest rates. A feedback loop arises, from which it is difficult to exit, and if no action is taken, this scenario will lead to stagflation. But what to do – it remains unclear.

It is apparent that the Bank of England has completed its rate-cutting cycle and is ready to embark on a rate-hiking cycle, albeit reluctantly, which is a factor favoring the strengthening of the pound. All other factors point to a weakening, as capital will flow to those regions of the world that will suffer the least from the energy shock and can provide decent returns with minimal risks. The UK is not one of those regions, so in the long term, if the war drags on, the pound has little room to strengthen.

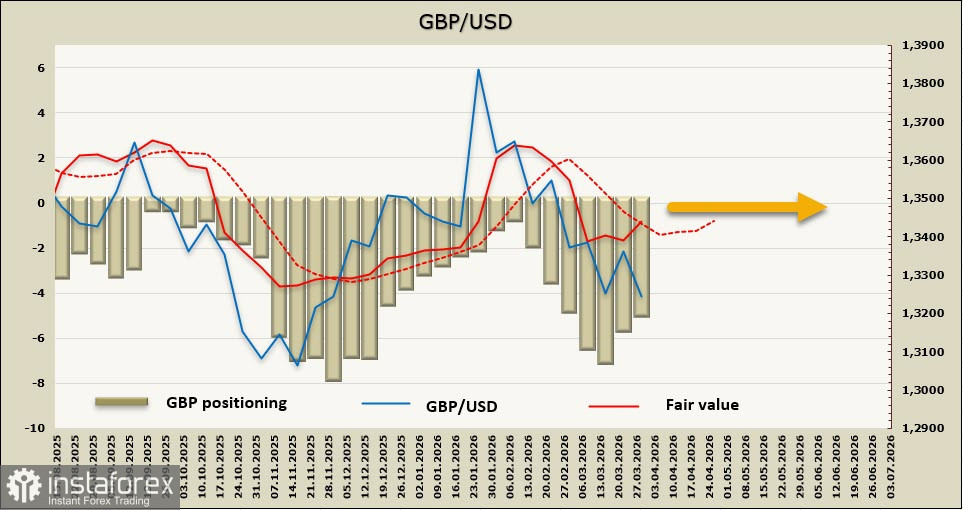

The net short position on GBP decreased by 0.6 billion over the reporting week to -4.9 billion, with positioning remaining bearish. The recalculated price, due to the bond correction following last week's failure, has returned to its long-term average, so the chances of continued growth are slim.

As we expected a week ago, after a brief correction, the pound headed down, updating its 3-month low. The target of 1.3000/50, which we previously saw as medium-term, is becoming increasingly closer. Unexpected news about a decrease in escalation in the Gulf could halt the decline, but the probability of such an event is diminishing. The market is gradually realizing that the crisis is not only not ending, but on the contrary, is acquiring increasingly global dimensions. A decline of the pound in the current conditions is the most likely scenario.